The Top 6 Dental Embezzlement Red Flags

Dental embezzlement red flags: what they mean, and what to do about them

First, let’s begin with a summary of the key points:

- An “embezzlement red flag” is an indicator of a circumstance that varies from “normal”. It shows that something is out of the ordinary and may need to be investigated further.

- An embezzlement red flag is simply a warning sign. A probability that the red flag is correlated with employee dishonesty.

- Red flags are a probability signal, and not proof that theft has occurred.

There are two categories to watch for:

- Behavioral Red Flags: identified by observing employee behaviors that are correlated with embezzlement

- Statistical Red Flags: unexplained discrepancies or variations in billing, payments and deposits over time.

How to interpret a red flag honestly

If you search the internet for the words “embezzlement red flags”, you’ll find dozens of articles and online resources dealing with the subject.

Most of the online red flag assessments I have viewed ask questions that require a binary Yes or No answer.

Here are a few of the red flag questions being asked:

- Does your employee have a wheeler-dealer attitude?

- Does your employee appear to have financial difficulties?

- Is your employee resistant to change or territorial?

These questions pose a problem, as they force you to choose between two options – either a yes or a no. A well designed embezzlement red flag questionnaire ask questions that do not force a binary answer and allow responses such as:

- Yes

- No

- Uncertain

- Does Not Apply.

Most embezzlement risk assessments (including my own) will assign point values to each response and calculate a total score at the end.

This is a good idea, but only when the scoring mechanism is understood, and the scores are for your own self-assessment.

Recently, I came across an embezzlement risk assessment questionnaire that predicted your risk of embezzlement in these four categories.

- Low score

- Embezzlement is unlikely, but still may happen.

- Medium score

- Perhaps embezzlement is happening.

- High score

- There is a good chance embezzlement is happening.

- Extreme score

- Almost certain embezzlement is happening.

This type of scoring is a sales tactic designed to inflate the threat. The questionnaire also included a “24 hour emergency hotline” to reach an expert to help you navigate the chaos. Just be sure to have your credit card handy when you call.

Consider this statement:

Fraud experts say that in 40% of embezzlement cases reported, the person stealing displayed a living standard disproportionate to their income.

This is how I like to think of it.

Let’s say you are convinced your employee is “living beyond their means” and you are unable to find a reasonable explanation to account for it; then there is a 40% chance that your employee’s enhanced lifestyle is the result of them stealing from you.

CONSIDER THIS NEXT STATEMENT

Fraud experts also report that in 20% of embezzlement cases, the perpetrator displayed “control issues”, or an unwillingness to share duties.

If you have a employee like this, then there is a 20% chance that your employee’s control freakishness is driven by behavior is a result the employee’s desire to “keep control” of things like the practice software and practice accounting for fear that you may uncover the theft.

Conversely, there’s an 80% chance that the employee’s behavior is linked to something else. Perhaps the employee is naturally OCD (like me) or trying to conceal their sloppy work that if discovered, would reflect poorly on their job performance.

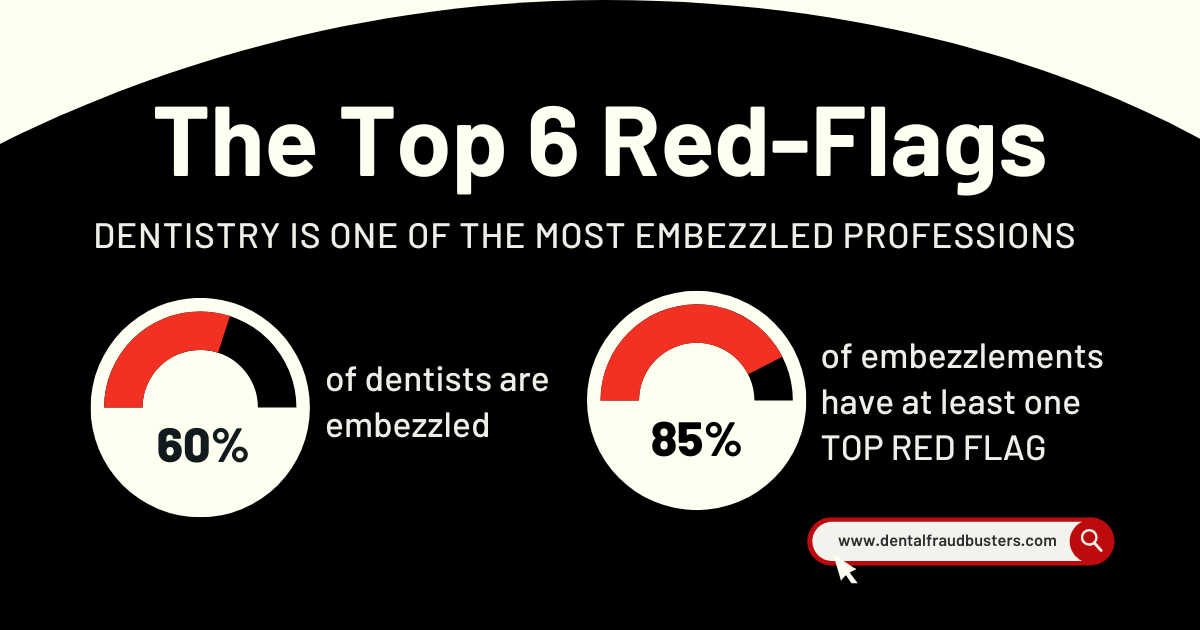

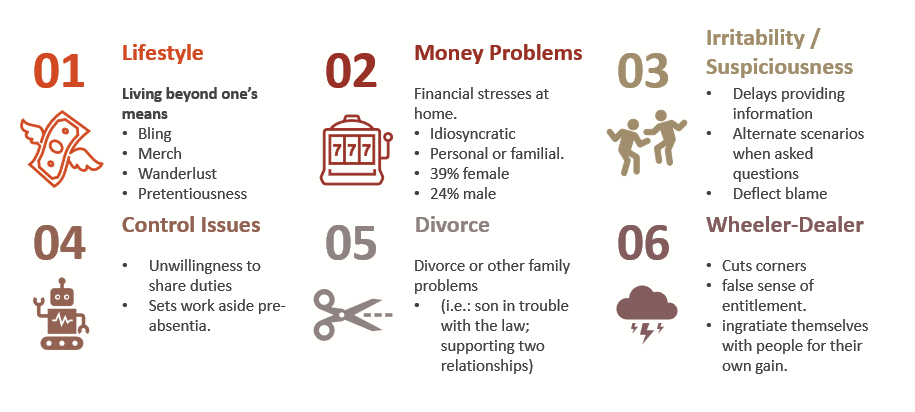

THESE are The TOP 6 Dental Embezzlement Red-Flags

At least one of these TOP 6 red flags was present in 85% of dental embezzlement cases.

The top 12 red flags, ranked by frequency

Research on confirmed embezzlement cases shows that at least one of the top six red flags was present in 85% of incidents. That said, each one also has a perfectly innocent explanation the majority of the time — context is everything.

| # | Red Flag | % of cases | Top 6 |

|---|---|---|---|

| 1 | Living beyond means | 40% | ★ |

| 2 | Financial difficulties | 34% | ★ |

| 3 | Wheeler-dealer attitude | 20% | ★ |

| 4 | Unwillingness to share duties | 19% | ★ |

| 5 | Divorce or family problems | 17% | ★ |

| 6 | Suspiciousness or defensiveness | 14% | ★ |

| 7 | Addiction problems | 13% | |

| 8 | Past legal problems | 9% | |

| 9 | Past employment problems | 8% | |

| 10 | Complaining about pay | 7% | |

| 11 | Refusal to take vacations | 7% | |

| 12 | Instability in life circumstances | 5% |

★ Top 6 flags were present in 85% of confirmed embezzlement cases.

CAN I check MY Practice for Embezzlement Red-Flags?

Yes, you can take our dental embezzlement self-assessment. Your responses are anonymous.

To learn more, click the button below.

What SHOULD I DO IF THERE IS A red-flag in my practice?

Remember – a red-flag is an indicator that fraud may be present; but it does not guarantee its presence. There may be an innocent explanation, but it may also point toward something more sinister.

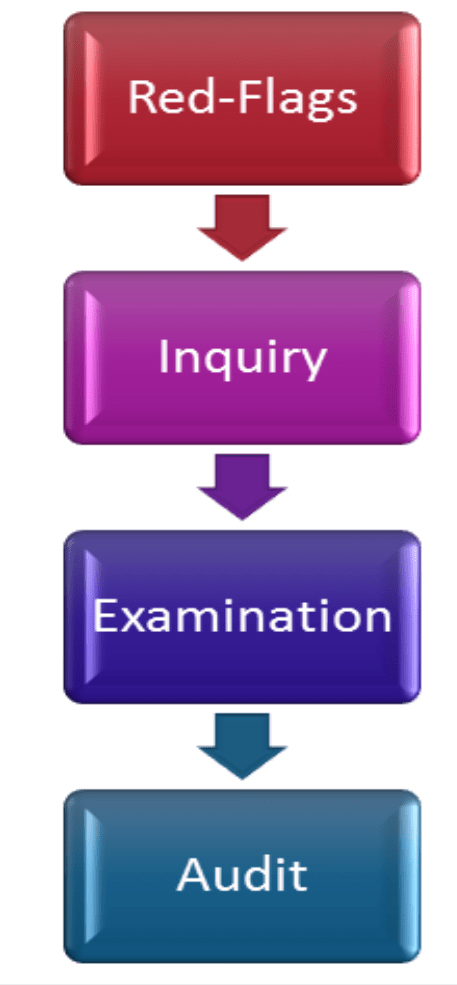

Do not ignore a red flag. The rule is – every red flag must be reasonably explained – follow the steps below:

Step 1: APPLY Skepticism

This is where you apply reason, logic and common sense.

Do not jump to conclusions.

(1) For each red flag that you observe, consider if there might be an alternate explanation, and the plausibility of that explanation being valid.

For example: if your employee is clearly “living beyond their means” and her explanation is “I had big win at the casino” – then this is likely to be a lie.

However, if you are aware that your employee recently received an inheritance or recently met a new partner with a solid W2, then that explanation more reasonable.

(2) When being asked to assess a red-flag, consider the question and the “weight” of your response.

Example: two dentists answered YES to this red-flag question:

Question: “Does your employee have financial pressures at home?”

- Dentist 1 answered yes based on the fact that the employee’s wages were recently garnished (or creditors were calling the practice, or practice loans were not repaid, etc.)

- Dentist 2 answered yes after overhearing the employee complaining to a co-worker about “how hard it is to make ends meet these days.”

Both dentists subjectively answered YES, however my feeling is that Dentist 1 should be more concerned than Dentist 2.

Step 2: CONDUCT A QUIET Inquiry

If careful reasoning cannot explain the red-flag you observed, then the next step is to conduct a quiet inquiry.

Ask yourself if other sources of information can be used to corroborate what you observed?

For example: If you are concerned that your employee is the first to arrive or last to leave each day (or comes in after hours to do work), then you can inquire further by checking your building alarm system and computer audit logs.

Most practices have an alarm system to that must be disabled when you enter, and enabled when you leave. Checking your building alarm log can tell you “how early” and “how late” your employee was coming and going.

Some employees will have a legitimate reason for coming to work early or staying behind. It could be that they started to use public transportation, or ride share to work with a friend who has to be at their job earlier – so your employee is dropped off at work earlier.

In situations like this, the employee will have a predictable pattern of arriving early to work around the same each day.

If an employee is coming in early or staying late in order to conceal embezzlement from you, then the patterns will vary. Some days the employee may not come in early or stay late, other days the employee will come in very early or work late.

Your alarm logs can also show if someone goes into the office after hours or on weekends.

If your alarm log shows your employee came in on Saturday night; check to see how long the employee was in the practice. If the employee stayed only for a few minutes, then likely they came by the office to pick something up that they left behind (like a wallet or cell phone).

If the employee stayed for an extended period of time, more than 10-15 mins, then it is more likely that they are up to no good.

You can also run an “audit report” from your practice management software to look for events that occur outside normal business hours. Most practice management software audit reports will show the date and time of events. Using those timestamps, look to see if things were happening when the office should have been closed.

If your own inquiry does not, or cannot remove your concerns, then consider the next step.

Step 3: CONSIDER A Diagnostic Examination

If you are unable to confirm a reasonable explanation for the red-flags or your suspicions remain strong, then a diagnostic examination of your practice’s computer data and business records to look for and identify evidence of embezzlement may be indicated.

If embezzlement is uncovered, the diagnostic examination will then estimate its scope and scale, so the practice owner can make informed (and important) decisions regarding recovery, restitution and possible prosecution.

As well, the diagnostic examination generally can provide the evidence required to terminate the perpetrator’s employment on a “for cause” basis, if they are still employed by the practice when the discovery is made.

Contact

William Hiltz BSc MBA CET

Hiltz & Associates

and the creator of

Dental FraudBusters.

Do you have questions regarding dental embezzlement, digital forensics or litigation support?

We welcome inquiries from dentists, dental specialists, practice owners, dental attorneys and consultants.

Get expert advice that is second to none.

Call, email, send a contact form or book a time online.

Initial consults are free.

Your inquiry is confidential and sent straight to William Hiltz.